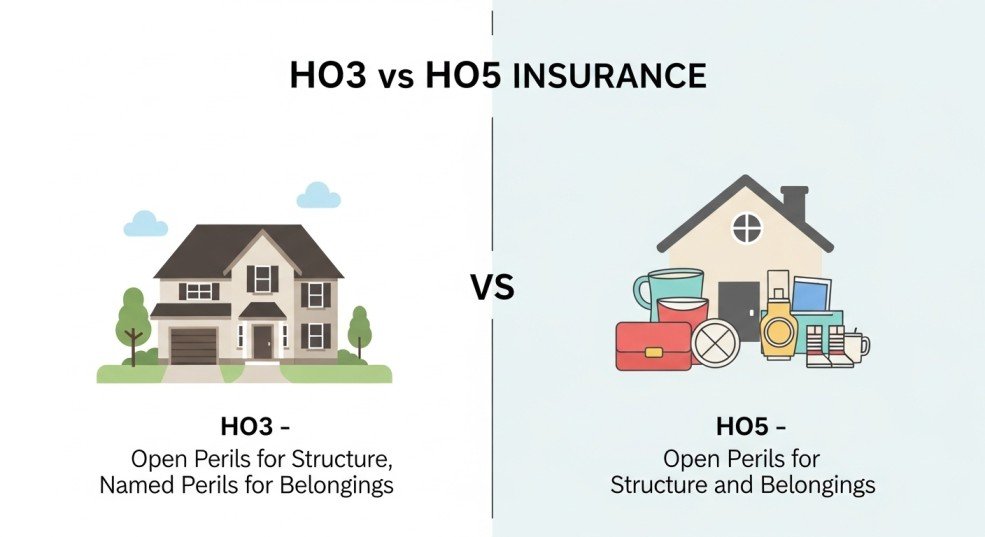

Quick Ans: The main difference between HO3 vs HO5 insurance policies is coverage scope. An HO3 policy covers your home structure on an open perils basis but protects personal belongings only for named perils. In contrast, an HO5 policy offers open perils coverage for both the structure and personal property, giving broader protection.

Many homeowners compare HO3 vs HO5 when choosing insurance coverage. Both policies protect your home. Both are widely used in the United States. However, they do not offer the same level of protection.

The confusion usually starts with the term “perils.” Some policies cover only specific risks. Others cover almost everything except listed exclusions. Because of this, homeowners often struggle to understand what is actually protected.

Choosing the wrong policy can lead to gaps in coverage. For example, you may assume your belongings are fully protected when they are not. As a result, unexpected losses can become costly.

Understanding HO3 vs HO5 helps you avoid these problems. It also helps you select the right policy based on your needs, budget, and risk level.

In this guide, you will learn clear definitions, advantages, disadvantages, real world examples, and practical exercises. By the end, you will confidently understand which policy suits you best.

Quick Answer: HO3 vs HO5

The difference between HO3 vs HO5 comes down to how risks are covered.

| Feature | HO3 Policy | HO5 Policy |

|---|---|---|

| Structure Coverage | Open perils | Open perils |

| Personal Property | Named perils only | Open perils |

| Coverage Level | Standard | Premium |

| Cost | Lower | Higher |

| Flexibility | Moderate | High |

In simple terms, HO5 provides broader protection than HO3, especially for personal belongings.

What Is an HO3 Policy?

An HO3 policy, also called a special form homeowners policy, is the most common type of home insurance.

It provides strong protection for the structure of your home. However, it limits coverage for personal belongings.

How HO3 Coverage Works

An HO3 policy uses two types of coverage:

- Open perils for the home structure

- Named perils for personal property

Open perils means everything is covered unless excluded. Named perils means only listed risks are covered.

Common Named Perils in HO3

Typical covered risks include:

- Fire and smoke

- Theft

- Vandalism

- Windstorms

- Hail

- Explosions

If a loss is not listed, it is not covered for personal property.

Example of HO3 Coverage

Imagine a pipe bursts in your home.

The structure damage is covered because it falls under open perils. However, personal items damaged by a cause not listed may not be covered.

Therefore, HO3 offers good protection but includes limitations.

What Is an HO5 Policy?

An HO5 policy, also known as a comprehensive form policy, provides the highest level of homeowners insurance coverage.

It protects both your home and belongings under open perils coverage.

How HO5 Coverage Works

With HO5:

- The home structure is covered under open perils

- Personal belongings are also covered under open perils

This means coverage applies unless the policy specifically excludes a risk.

Common Exclusions

Even HO5 policies exclude certain risks, such as:

- Floods

- Earthquakes

- Wear and tear

- Neglect

However, compared to HO3, coverage is much broader.

Example of HO5 Coverage

Suppose your laptop is accidentally damaged.

In many cases, HO5 may cover the loss unless the cause is excluded. This broader protection makes HO5 attractive for homeowners with valuable belongings.

Key Differences Between HO3 vs HO5

Coverage Scope

The biggest difference in HO3 vs HO5 is coverage scope. HO3 limits personal property coverage to named perils. HO5 covers most risks unless excluded.

Simplicity

HO5 policies are easier to understand. Everything is covered unless excluded. HO3 requires checking a list of covered risks.

Cost

HO5 policies cost more because they offer broader protection. HO3 policies are more affordable but provide less coverage.

Eligibility

HO5 policies are often available only for well maintained homes in low risk areas. HO3 policies are more widely available.

Advantages and Disadvantages

HO3 Advantages

- Lower premium cost

- Widely available

- Good structural protection

HO3 Disadvantages

- Limited personal property coverage

- More complex claims process

- Potential coverage gaps

HO5 Advantages

- Comprehensive protection

- Easier to understand coverage

- Better protection for valuables

HO5 Disadvantages

- Higher cost

- Limited availability

- Stricter eligibility requirements

Choosing between HO3 vs HO5 depends on your budget and coverage needs.

Real World Examples

Scenario 1: Theft

If someone steals your electronics:

- HO3 covers the loss only if theft is listed

- HO5 covers the loss unless excluded

Scenario 2: Accidental Damage

If you accidentally damage furniture:

- HO3 may not cover it

- HO5 is more likely to cover it

Scenario 3: Natural Damage

If a storm damages your home:

- Both HO3 and HO5 typically cover structural damage

- HO5 may provide broader protection for contents

These examples show how HO3 vs HO5 affects real life situations.

Regional and Global Usage

United States

HO3 policies are the most common homeowners insurance type. HO5 policies are considered premium coverage options.

Other Countries

Insurance systems differ globally. However, similar concepts exist, where some policies offer limited coverage and others provide broader protection.

Market Trends

Many homeowners upgrade from HO3 to HO5 as their assets increase. Higher value homes often qualify for HO5 policies.

Related Concepts and Comparisons

HO3 vs HO2

HO2 policies provide named perils coverage for both structure and belongings, offering less protection than HO3.

HO5 vs HO3 vs HO2

| Feature | HO2 | HO3 | HO5 |

|---|---|---|---|

| Structure Coverage | Named perils | Open perils | Open perils |

| Personal Property | Named perils | Named perils | Open perils |

| Coverage Level | Basic | Standard | Premium |

Understanding these policy types helps clarify the HO3 vs HO5 comparison.

Common Mistakes About HO3 vs HO5

Assuming All Damage Is Covered

Many homeowners assume HO3 covers everything. In reality, personal property is limited to named perils.

Ignoring Policy Exclusions

Even HO5 does not cover everything. Floods and earthquakes are usually excluded.

Choosing Based Only on Price

Lower premiums may lead to insufficient coverage. Always compare protection levels.

Not Reviewing Coverage Regularly

As property value increases, upgrading from HO3 to HO5 may be necessary.

Avoiding these mistakes ensures better insurance decisions.

Beginner to Advanced Tips

Beginner Level

Start by understanding the difference between named and open perils.

Intermediate Level

Review your personal property value and risks.

Advanced Level

Compare multiple insurance providers and customize coverage with endorsements.

Better knowledge leads to smarter choices in HO3 vs HO5 policies.

Step By Step Decision Scenario

Imagine you are choosing insurance for your home.

If you select HO3:

- Review named perils list

- Check personal property limits

- Consider additional coverage

If you select HO5:

- Review exclusions

- Confirm eligibility

- Evaluate higher premium

This process helps you make an informed decision.

Exercises With Answers

Exercise 1

Which policy provides open perils coverage for personal property?

Answer: HO5.

Exercise 2

Which policy is more common?

Answer: HO3.

Exercise 3

Which policy offers broader protection?

Answer: HO5.

Exercise 4

Which policy is usually cheaper?

Answer: HO3.

Exercise 5

True or False: HO5 covers fewer risks than HO3.

Answer: False.

When Should You Choose HO3 vs HO5?

Choose HO3 if you:

- Want lower premiums

- Have fewer valuable belongings

- Prefer basic coverage

Choose HO5 if you:

- Want maximum protection

- Own high value items

- Prefer simple coverage terms

Your decision should match your financial situation and risk tolerance.

FAQs About HO3 vs HO5

What is the main difference between HO3 vs HO5?

HO3 covers personal property for named perils only, while HO5 provides open perils coverage for both structure and belongings.

Is HO5 better than HO3?

HO5 offers broader protection, but it also costs more. The best choice depends on your needs.

Why is HO5 more expensive?

HO5 costs more because it covers more risks and provides higher protection.

Can I upgrade from HO3 to HO5?

Yes. Many insurers allow upgrades if your home meets eligibility requirements.

Does HO5 cover everything?

No. Some risks like floods and earthquakes are still excluded.

Which policy is more common, HO3 or HO5?

HO3 is more common because it is more affordable and widely available.

Is HO3 enough for most homeowners?

HO3 is sufficient for many people, but it may not cover all personal property risks.

Do both policies cover the home structure?

Yes. Both HO3 and HO5 provide open perils coverage for the structure.

How do I know which policy I need?

Evaluate your belongings, budget, and risk level before choosing.

Is HO5 worth the extra cost?

For homeowners with valuable property, HO5 can be worth the higher premium.

Conclusion

Understanding HO3 vs HO5 is essential for choosing the right home insurance policy. Both options protect your home, but they differ in coverage level and flexibility.

HO3 policies offer strong structural protection and lower premiums. However, they limit coverage for personal belongings. HO5 policies provide broader protection by covering both structure and personal property under open perils.

Although HO5 costs more, it reduces coverage gaps and simplifies claims. Therefore, it suits homeowners who want comprehensive protection.

Budget and risk tolerance should guide your decision. If you want basic coverage at a lower cost, HO3 is a practical choice. If you prefer maximum protection and fewer limitations, HO5 is the better option.

Careful comparison ensures you choose the right policy for your needs.

Discover More:-

- Springtail vs Flea: Differences, Identification, and Control Guide

- Yuca vs Yucca: Differences, Uses, Benefits, and Complete Guide

Lisa Thompson is a USA-based content writer and language specialist focused on grammar, writing improvement and digital publishing.

She holds a degree in English Language and Communication and has professional experience in educational and web content creation.

As the author of Gramtivo.Com, she aims to help readers improve their writing skills through clear and practical guidance.

Pingback: Coaches or Coach’s: Difference, Rules, and Easy Grammar Guide